The Ultimate Guide to CBDCs: Everything You Need to Know

Are you curious about the latest advancements in digital currencies? Then you need to know about CBDCs – the newest frontier that's creating a buzz in the financial world with their potential to revolutionize the way we conduct transactions and manage our money.

But what exactly are CBDCs, and how do they work? That's where this ultimate guide comes in. In this post, we'll break down everything you need to know about CBDCs, from their definition and purpose to how they work and their potential impact on the future of finance. Get ready to become an expert on this exciting new development in the digital currency world!

TABLE OF CONTENT

- What are CBDCs?

- What are the goals of CBDCs?

- What types of CBDCs are there?

- What’s the difference between a CBDC and a cryptocurrency?

- What are the pros and cons of CBDCs?

- What are the prospects for CBDCs?

- How to prepare for CBDC adoption?

What are CBDCs?

The world is rapidly moving towards a digital future, and it's no surprise that many countries are adopting Central Bank Digital Currencies (CBDCs) as a way to modernize their financial systems. CBDCs are a form of digital currency that is issued and backed by a country's central bank, with its value equivalent to the country's fiat currency.

But where did the concept of CBDCs come from? The idea of digital currency has been around for years, with the emergence of cryptocurrencies like Bitcoin and Ethereum in the late 2000s. These decentralized currencies gained popularity because of their ability to provide secure, transparent, and decentralized transactions without relying on traditional financial institutions.

As interest in cryptocurrencies grew, central banks began to explore the idea of creating their own digital currencies. In 2014, the Central Bank of Ecuador became the first central bank to launch a digital currency, and the Central Bank of Tunisia followed suit in 2015. Since then, many countries, including China, Sweden, and the Bahamas, have either launched or are in the process of developing their own CBDCs.

Overall, CBDCs represent an exciting development in the world of digital currencies, with the potential to revolutionize the way we think about and use money. As more countries explore the idea of CBDCs, it will be fascinating to see how this technology evolves and what impact it will have on the future of finance. Stay tuned for more updates and exciting developments in the world of CBDCs.

What are the goals of CBDCs?

When it comes to Central Bank Digital Currencies (CBDCs), it's important to understand that they are not all created equal. The research and development process for CBDCs is influenced by several key goals that are unique to each digital currency. In this section, we'll take a deeper dive into the primary policy goals that have been identified by different jurisdictions.

Financial inclusion is a key policy goal for CBDCs. It aims to increase access to appropriate and affordable financial services, which can lead to poverty reduction worldwide. With CBDCs, financial inclusion could be achieved by enhancing access to digital payments, thus acting as a gateway to wider access to financial services.

Access to payments is crucial for countries facing challenges like a shortage of cash or lack of digital infrastructure. CBDCs could potentially help achieve universal access to payments, especially for individuals in remote areas where private firms find it unprofitable to operate.

CBDCs could make payments more efficient and cheaper to operate, as central banks could offer low-cost payments as a public good. Additionally, ensuring the resilience of payments is important, especially for countries in disaster-prone areas where natural disasters could result in destruction of physical and financial infrastructure.

CBDCs could also reduce the illicit use of money by addressing the anonymity and lack of an audit trail associated with cash. Moreover, CBDCs could secure monetary sovereignty in a digital future and increase competition in a country's payments sector by competing with existing forms of payments or by designing the CBDC platform as open to private payment service providers.

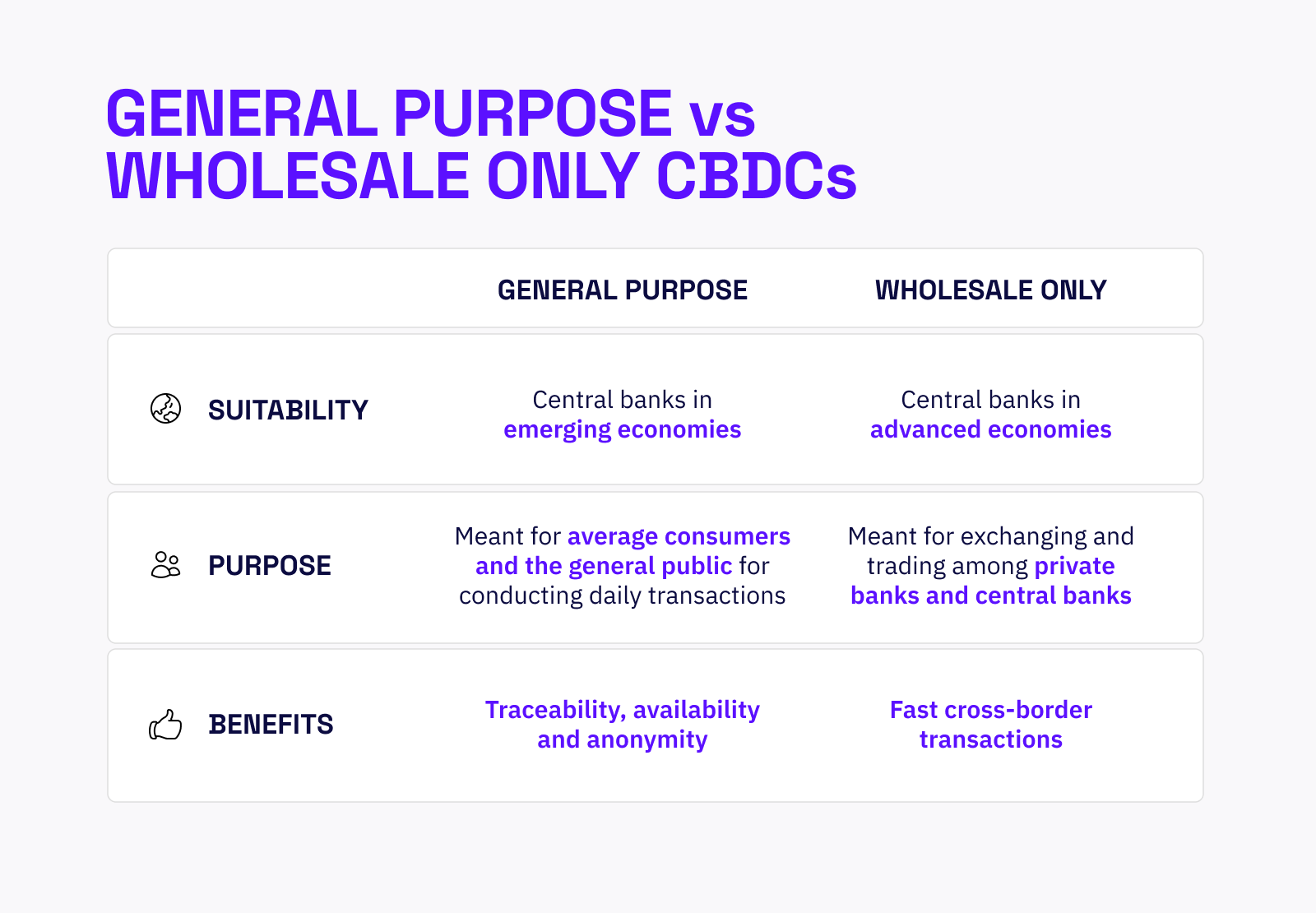

What types of CBDCs are there?

The first type of CBDC is the general-purpose CBDC, which is distributed to the general public. This type of CBDC has several features, such as anonymity, traceability, and availability 24/7. It also has the potential for an interest rate application, making it an attractive option for central banks in emerging markets. General-purpose CBDCs can promote financial inclusion and reduce currency printing and handling costs.

The second type of CBDC is the wholesale-only CBDC, which is designed for banks that keep reserve deposits with a central bank. It aims to increase the efficiency of payments and securities settlements and reduce counterparty credit and liquidity risks. The wholesale CBDC uses a restricted-access digital token, which replaces or supplements central bank reserves. This system is faster, cheaper, and safer than the current wholesale financial systems, making it an attractive option for central banks.

Understanding the different types of CBDCs is essential to understand the future of digital currencies. The infographic below will provide a visual representation of the differences between retail and wholesale CBDCs.

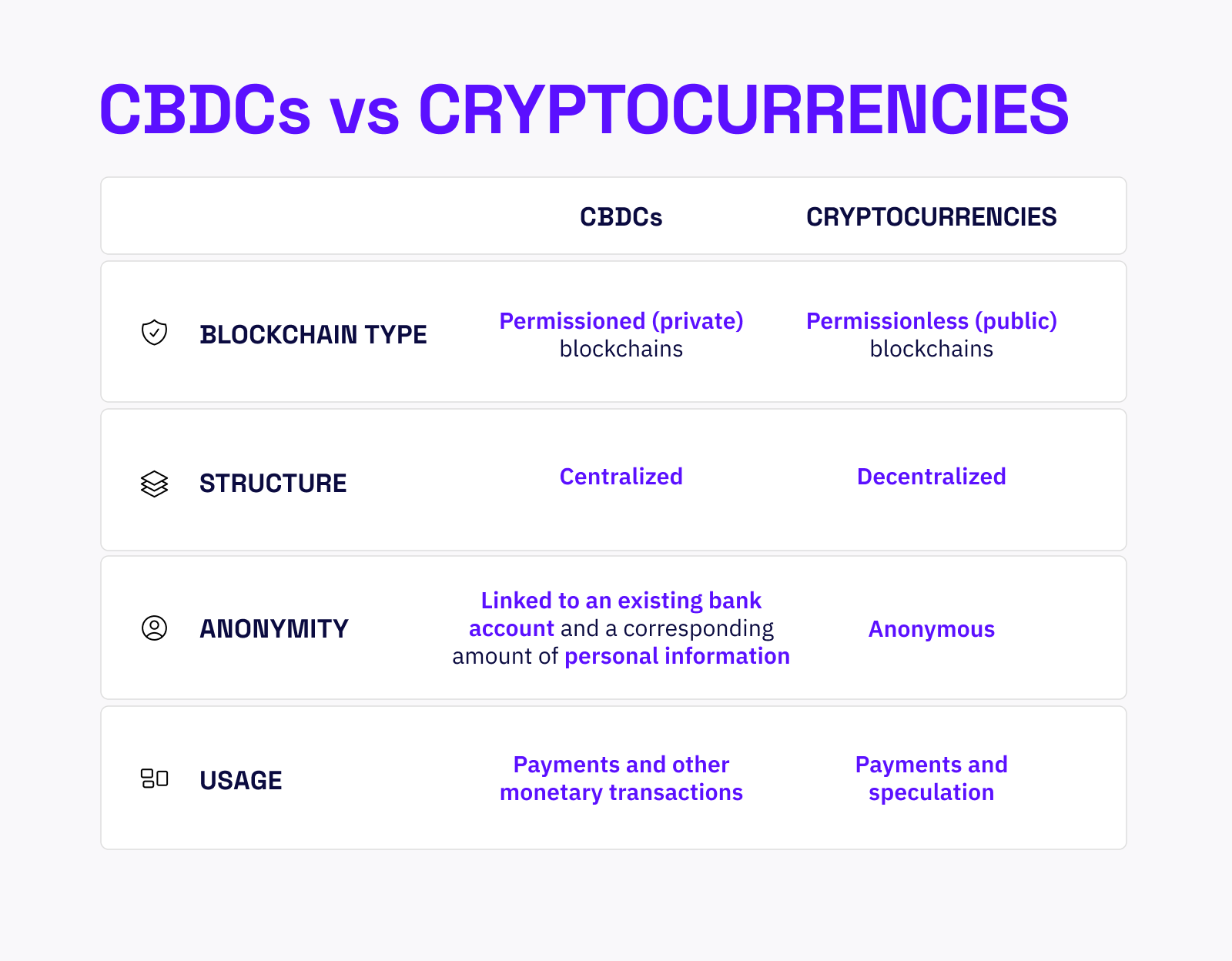

What’s the difference between a CBDC and a cryptocurrency?

CBDCs are digital currencies issued by central banks that have central banks at the heart of every transaction. In contrast, cryptocurrencies like Bitcoin are digital tokens created using cryptographic methods by a distributed network or blockchain. CBDCs use permissioned (private) blockchains, while cryptocurrencies employ permissionless (public) blockchains, which allow anyone to join and participate in the blockchain network's essential operations. As a result, public blockchains can self-govern.

Centralization is the most significant distinction between the two. CBDCs are centralized, while cryptocurrencies are decentralized. Central banks are in charge of regulating CBDC transactions, while cryptocurrencies are based on a consensus of users. Anonymity is another key difference; while cryptocurrencies offer anonymity, CBDCs allow central banks to see who owns what.

CBDCs are more likely to run on distinct technological platforms than cryptocurrencies, which often use blockchain. Unlike stablecoins, which are pegged to a fiat currency like the U.S. dollar, a CBDC would be the fiat currency itself, such as a CBDC dollar bill, which is identical to a regular dollar bill.

CBDCs can only be used for payment, while cryptocurrencies can be used for both financial transactions and speculation purposes. CBDCs offer several benefits, such as better control of the monetary system, reduced risk of a third party, and increased financial inclusion. They are less concerned about data and privacy than cryptocurrencies; however, users can choose how much and what kind of data they want to disclose, as cryptocurrencies are peer-to-peer. In contrast, CBDC transactions automatically send vast amounts of data to tax and regulatory agencies.

What are the pros and cons of CBDCs?

On the positive side, CBDCs can make monetary policy and government functions easier to implement, reducing work and processes by automating transactions between banks and customers. They also eliminate third-party risks, as the central bank takes full responsibility for the remaining risks in the system.

Privacy is another advantage, with retail CBDCs protecting personal information through anonymous transactions, while account-based access works like a traditional bank account and can include privacy protections. Additionally, CBDCs can deter illegal activities due to their digital storage and traceability, making it easier for the central bank to monitor and prohibit criminal activity.

Furthermore, CBDCs can provide a direct link between customers and central banks, bypassing the need for costly infrastructure and thus promoting financial inclusion for the unbanked population in developing nations.

On the other hand, CBDCs are not always the solution to centralized financial systems. The central bank retains the authority to conduct transactions, which could affect the data and transaction levers between citizens and banks. Moreover, privacy concerns arise, as every transaction is visible to the service provider, raising potential issues similar to those experienced by IT giants and ISPs.

Cross-border payments can also be a challenge, as different legal and regulatory frameworks create considerable barriers. Additionally, CBDCs may have unintended effects on foreign exchange markets, with China's CBDC aiming to threaten the dollar's dominance. If the digital yuan becomes the primary payment tool in China, it could affect the dollar's role, potentially causing global companies to use it for business.

In conclusion, while CBDCs bring many benefits to the table, they are not without their challenges. It will be up to central banks to weigh the pros and cons and decide whether CBDCs are the right path forward for their respective countries.

What are the prospects for CBDCs?

The current fractional reserve system allows banks to create money by lending out more than they have in liquid deposits. However, with the introduction of CBDCs, banks will have to shift to a "loanable funds intermediary" model. This means they will have to borrow long-term funds to finance long-term loans like mortgages, which would result in a more secure financial system.

The benefits of CBDCs are many. They will help prevent bank runs and give central banks more control over private banks' credit/lending choices. In addition, CBDCs will be a secure and impartial payment and settlement asset, acting as a shared interoperable platform for the new payment ecosystem.

A well-designed CBDC system will create an integrated open finance architecture that welcomes competition and innovation, which will ultimately benefit consumers. It will also maintain democratic control over the currency, ensuring that everyone has a say in the future of the monetary system.

The road ahead for CBDCs is exciting and full of possibilities. With the introduction of this revolutionary system, we can expect to see significant changes in the financial landscape. It's time to prepare for the future and embrace the power of CBDCs.

How to prepare for CBDC adoption?

As we've discussed, the potential adoption of CBDCs could result in mass adoption for the blockchain industry as a whole, bringing about exciting investment opportunities. But how can you prepare for this new wave of investment potential? Here are a few tips to help you get started.

First and foremost, it's essential to do your research. Look into top projects in the industry that align with your values, and make sure they are legitimate and safe before investing in them. This will help you make informed investment decisions and avoid potential risks.

Additionally, with the current market being in a bearish trend, it's an excellent opportunity to invest in promising projects at lower prices. But it's essential to manage your risk and maintain a diverse portfolio that includes both safe, stable assets and some riskier but potentially more profitable ones.

To explore new financial services, consider options like Staking, Liquidity Mining, and Lending to get creative with your portfolio. There are several platforms available that can help you navigate these new investment opportunities.

At Cake DeFi, we offer a comprehensive platform that can assist you in all of the above with the highest degree of transparency. We know how to make your crypto work for you. So why not sign up today and start exploring everything we have to offer?